Reporting is a critical component of effective financial management. It’s the culmination of your nonprofit’s other accounting, bookkeeping, and strategic activities—where you organize the data you’ve collected so it’s more useful for internal decision-making and external accountability.

Among the most important reports you’ll create each year are a set of four financial statements: the statements of activities, financial position, cash flows, and functional expenses. Each of these reports summarizes different financial data so you can draw unique, actionable insights from them.

In this guide, you’ll learn all you need to know about nonprofit financial statements, including:

Before we dive into the details of each statement, let’s get started by discussing why your organization needs to compile these reports.

Your organization primarily needs to create financial statements to comply with nonprofit regulations. Not only will compiling your data in these formats help you accurately file your annual tax returns with the IRS, but financial statements are also required under the Generally Accepted Accounting Principles (GAAP), a set of regulations that standardize accounting practices across all for-profit and nonprofit organizations.

However, just because your nonprofit has to create these reports doesn’t mean they aren’t useful in other ways! Financial statements can also be helpful for:

These additional benefits of financial statements are why it’s important for everyone at your nonprofit to have at least some understanding of the data they contain. When your organization’s leadership, fundraisers, program staff, and other team members are all financially literate and reference reports as they go about their daily tasks, financial management truly works alongside your other activities to further your mission.

Now that you understand the overall importance of financial statements, let’s look more closely at the individual reports. We’ve included a template in each section to help you create your own statements, plus links to examples from real nonprofits you can model yours off of.

The nonprofit statement of activities is similar to what for-profit organizations call an income statement or profit and loss report. It essentially outlines your organization’s major transactions for the year to provide a detailed overview of spending and revenue generation.

Each nonprofit financial statement has three major sections, and the three divisions of the statement of activities include:

The line items in your revenue and expense sections of your statement of activities should match those in your nonprofit’s annual operating budget. Budgeting is the internal process where your statement of activities is most applicable, since you can compare your actual spending and fundraising numbers from the end of the year to your projections from the beginning of the year. Then, you can use this information to make more accurate predictions in next year’s budget.

For a strong real-world example of a statement of activities, check out the World Wildlife Fund’s 2024 annual report.

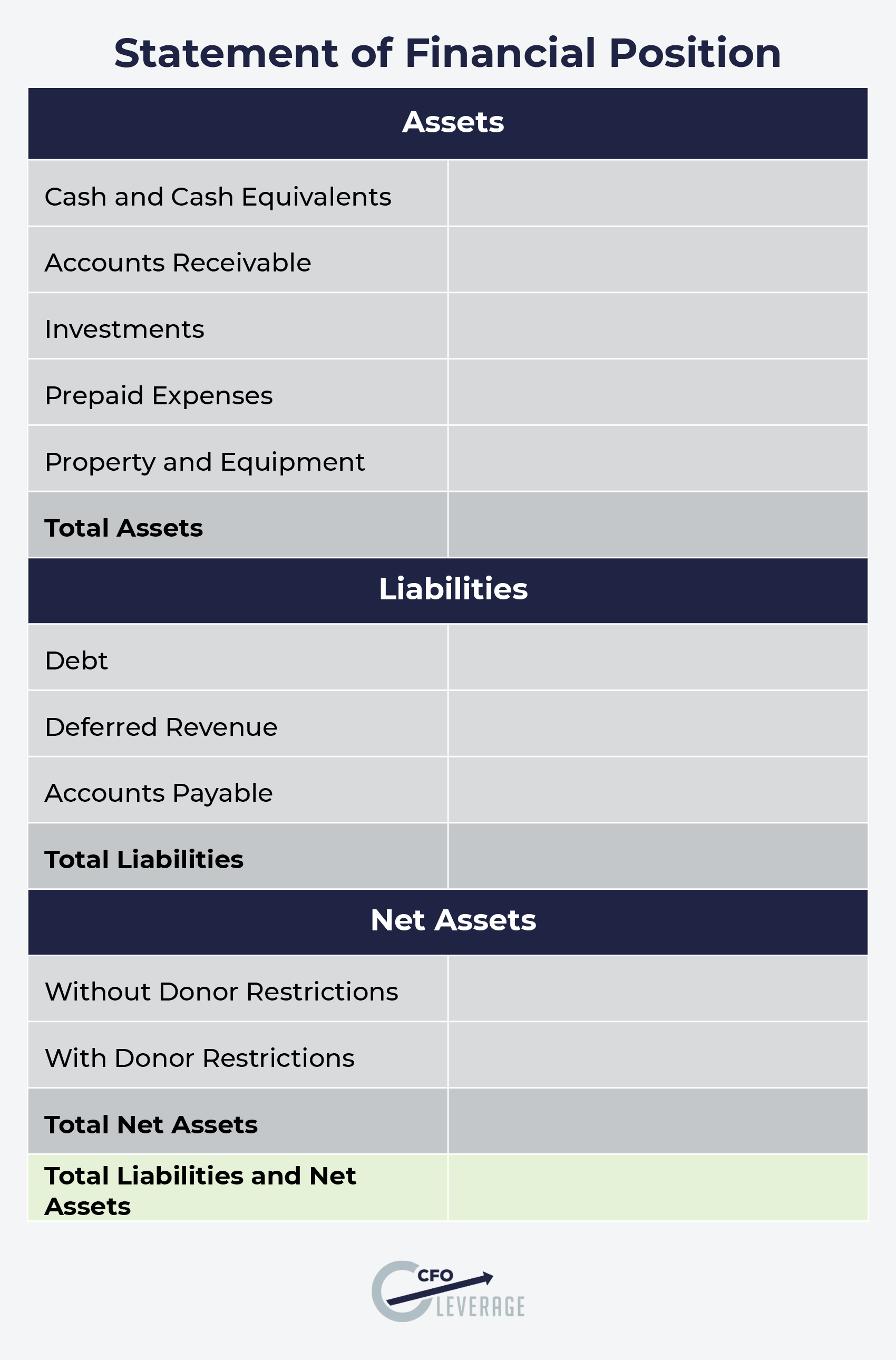

You might have heard the statement of financial position called a “balance sheet,” and the two terms are interchangeable in the nonprofit sector (businesses tend to prefer the latter). Either way, this report provides a snapshot of your organization’s financial health, growth potential, and general sustainability.

The three sections of a nonprofit statement of financial position include:

Your statement of financial position can help you determine several essential components of your nonprofit’s health and sustainability, such as:

Because of these applications, balance sheets play a central role in most financial audits, meaning you can learn even more about your financial health and position through them.

For a strong real-world example of a statement of financial position, check out The Nature Conservancy’s 2024 annual report.

The statement of cash flows has the same name in both for-profit and nonprofit contexts, as well as the same general purpose: to show how cash moves in and out of an organization. Its three sections correspond to different types of spending and revenue generation activities as follows:

Most organizations pull statements of cash flows each month instead of just once a year. This way, they’re more useful for keeping your spending and fundraising on track with your budget and letting you know where you might need to make adjustments. Plus, understanding regular movement of cash helps you avoid overdrafting your nonprofit’s bank accounts.

For a strong real-world example of a statement of cash flows, check out Habitat for Humanity’s 2024 consolidated financial statements.

The statement of functional expenses is the one financial statement that only nonprofits create. This is because it categorizes your organization’s spending according to how it furthers your mission, which ties back to the unique goal of nonprofit accounting—remaining accountable to stakeholders and your commitment to making a difference as you manage your finances.

The statement of functional expenses is usually laid out as a table or matrix. The row labels show natural expense categories, which describe the nature of each cost and are how you would typically record an expenditure in your accounting system (e.g., “mortgage payments” or “marketing material creation”). The column labels show the three categories of functional expenses, which are more mission-driven. They include:

Functional expense categorization is required on IRS Form 990, so this report will be especially helpful come tax season. However, you can also use it throughout the year for evaluating how productively you’re using your resources.

In the past, the general rule was for at least 65% of nonprofits’ spending to be program-related and no more than 35% to go toward overhead. While it’s now understood that the exact breakdown will look different for every organization, you should still ensure that the majority of your expenditures directly further your mission. If you need to cut costs to balance your budget, always try to reduce overhead spending before taking funding away from programming.

For a strong real-world example of a statement of functional expenses, check out Furkids Animal Rescue & Shelters’ 2023 audited financial statements.

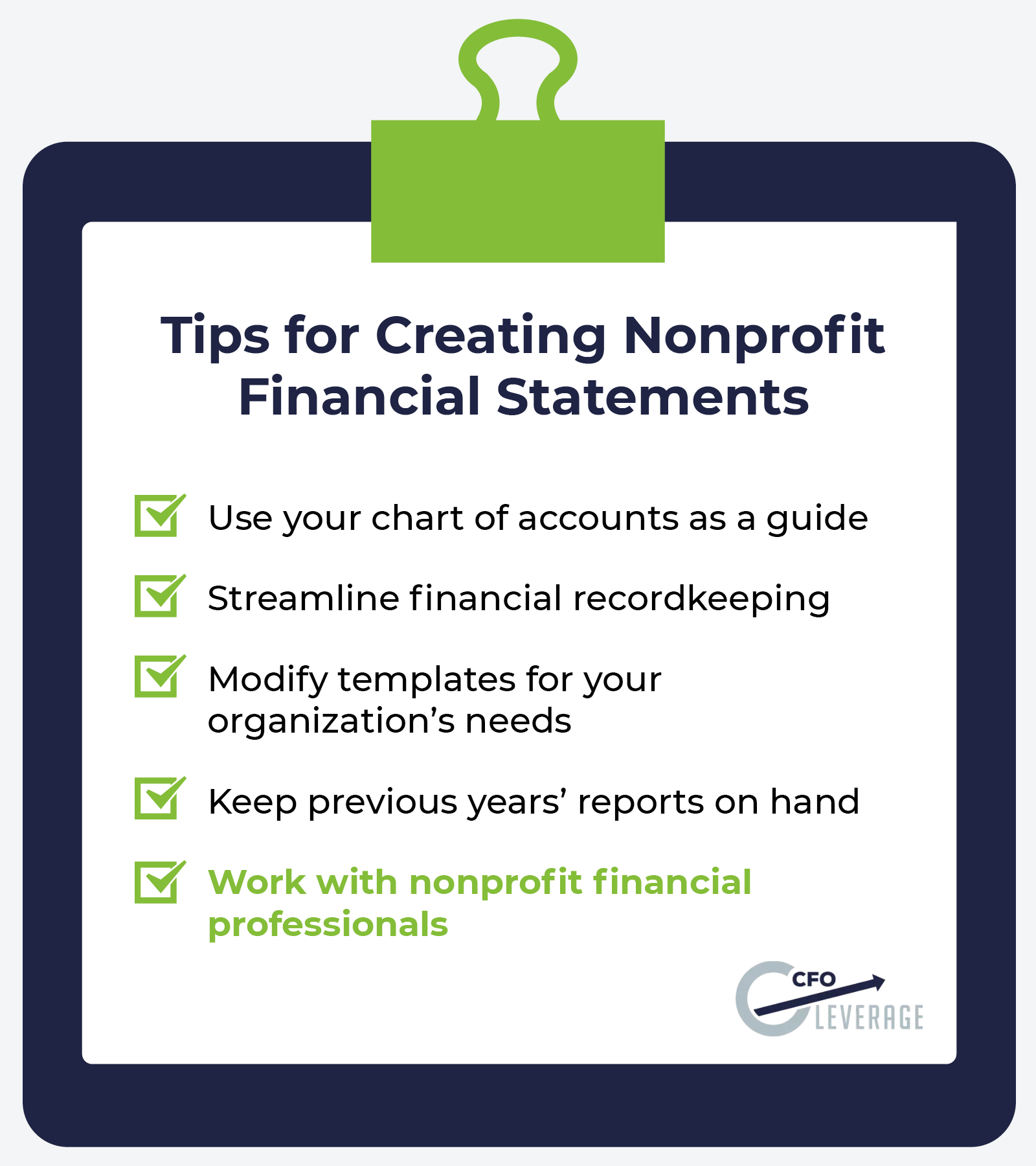

While the overviews, templates, and examples above should provide a solid foundation for understanding the four core nonprofit financial statements, you might still be wondering about the best ways to create them. Here are a few tips to help you get started:

If you still have questions or need help creating and analyzing your financial statements, turning to nonprofit financial professionals—like our team at CFO Leverage—is your best bet. From everyday recordkeeping and restricted fund management to cash flow tracking and budgeting support, our affordable, comprehensive services will put your organization on the right track for effective reporting and decision-making. We also work exclusively with nonprofits, so we understand your statements well and can interpret them to develop effective financial strategies.

Financial statements are essential for effective nonprofit accounting and management, far beyond their compliance purposes. Keep accountability and transparency at the forefront as you compile your organization’s reports to ensure they’re as accurate and useful as possible, and make sure everyone at your nonprofit is on the same page about how to apply the information they contain for maximum effectiveness.